You are using an outdated browser. Please upgrade your browser to improve your experience.

No results found

Try adjusting your search to see more results.

A company can partner with Smart Money People and invite their verified customers to leave a review. When they do this it’s labelled as "Verified source" on the Smart Money People website.

There are a number of automated invitation techniques available to businesses. All of which are trusted and ensure that only verified customers can leave reviews through them.

Santander: Travel Insurance reviews

No new 5 star reviews, no new 1 star reviews, latest highest rating:.

Latest lowest rating:

About the Travel Insurance

Santander travel insurance reviews can help you to find our what other customers really think! We all know that there are hundreds of different travel insurance policies on the market, all designed to help you stay protected while travelling...and giving you piece of mind, whether you're enjoying a sun swept beach or on an adventure-packed holiday. But with so many different policies to choose from, finding the right policy for you can be quite confusing. Reading our Santander travel insurance reviews can help you find out what other travellers have to say. You can also write your Santander travel insurance review too!

Review Santander: Travel Insurance now

Santander travel insurance reviews ( 7 ), no payment, drones at gatwick - no insurance payout.

Very complicated process but good price

Extremely poor customer service

Showing 4 of 7

Do you have a different Santander product?

There's still more to see!

Join smart money people.

Keep up to date on ratings of your favourite businesses. Find out about our awards and write new reviews with ease

News, guides and insight from our team

The impact of not collecting customer reviews

First time buyer guide to mortgages: what you should know before buying a property

.png "santander 123 benefits travel insurance")

The hidden costs of home ownership

How customer reviews can help with SEO

Santander Travel Insurance for Private Banking clients

As voted by The Times Money Mentor Awards 2023

Welcome to your discount on Santander Travel Insurance. As a Santander Private Banking client, you’re entitled to 35% discount on all our travel insurance policies, when you apply online.

To make sure your discount is applied, you must quote and apply from this page . The discount will then automatically be applied to your price.

Wherever you are travelling to, have a safe and happy trip.

- Family, couple or individual policy

For full details of the cover available, including any exclusions, please take a look at the Santander Travel Insurance policy documentation Several optional cover extensions, for example Winter Sports Cover, are available for an additional premium. You’ll be able to find out more about each of these when you get a quote. 35% online discount as a Private Banking client will also apply to any optional cover extensions you may need.

If you stop being a Private Banking client during the term of the travel insurance policy, we reserve the right to withdraw the discount applied for the remaining period of cover.

This offer is subject to availability.

The online price is 35% less than the telephone price for Santander Private Banking clients.

This discount applies to the main policy and to any optional cover extensions you may choose to buy.

You need to apply online to get your discount. Cover provided by Chubb.

However, if you would prefer to apply over the phone, please call Chubb on 0800 519 9921 . Opening hours are Monday to Friday 9am to 5pm

COVID cover you have with a Santander Travel Insurance policy

- Cancellation costs, including pre-booked excursions, if you (or someone you are travelling with) have COVID or are told to self-isolate and you miss your holiday.

- Medical expenses if you get COVID on holiday overseas.

- Travelling home and additional accommodation costs if you get COVID or have to self-isolate and can’t return home on time.

A positive COVID test result must be verified. See our policy document for full details.

What’s not covered You won’t have any COVID cover if the Foreign, Commonwealth & Development Office (FCDO) has advised against travelling to your destination. You’re also not covered:

- for costs you can claim back from anywhere else (including a credit from your travel provider)

- if you decide not to travel

- if you can’t travel due to restrictions put in place by your travel provider, any government, or any country

- for financial failure of your travel provider.

Always check before booking a trip

Before booking a trip or travelling, check the FCDO website for travel advice. You can check the country you plan to visit for the latest updates and whether it's safe to go there. These updates can change regularly and at short notice. We strongly recommend that you check your cancellation rights with your travel provider before booking a holiday abroad.

Please read our travel insurance policy documents for the terms and conditions. These give full details of what's covered, and any excesses and exclusions that may apply.

State of Play. 18 April 2024

State of play. 4 april 2024, state of play. 21 march 2024, state of play. 7 march 2024, state of play. 22 february 2024, state of play. 15 february 2024, quarterly perspectives - february 2024.

One of our core team will be happy to discuss your unique needs from a private bank.

Santander Travel Insurance Review

Marvin's low-down on Travel Insurance from Santander UK plc

The experts say:

What santander uk plc customers are saying right now:.

- 😀 Able to move £25k per day with no problem.

- 👍 Easy access saver interest rate increased in line with BOE rate rise.

- 👌 App does not crash like some other banks.

- 😌 Log in security questions answered quickly and successfully.

- 😍 Customer service described as "lovely" and "brilliant".

- Terrible customer service 🤬

- Inconvenient account opening process 🤯

- Unhelpful and unresponsive staff 😡

Santander customer reviews summary

Santander has been receiving a lot of negative reviews lately for their customer service and general operations (though it's important to note that many of these are not travel insurance related). Customers have reported long wait times to speak with customer service, blocked payments, and difficulties transferring money. Despite this, some customers have praised the bank for having quick response times and raising the interest rate on their easy access saver account shortly after the Bank of England raised its rate. Overall, Santander UK plc's customer service and banking operations leave a bit to be desired, earning it a score of 6/10.

Deep-dive into Santander Travel Insurance

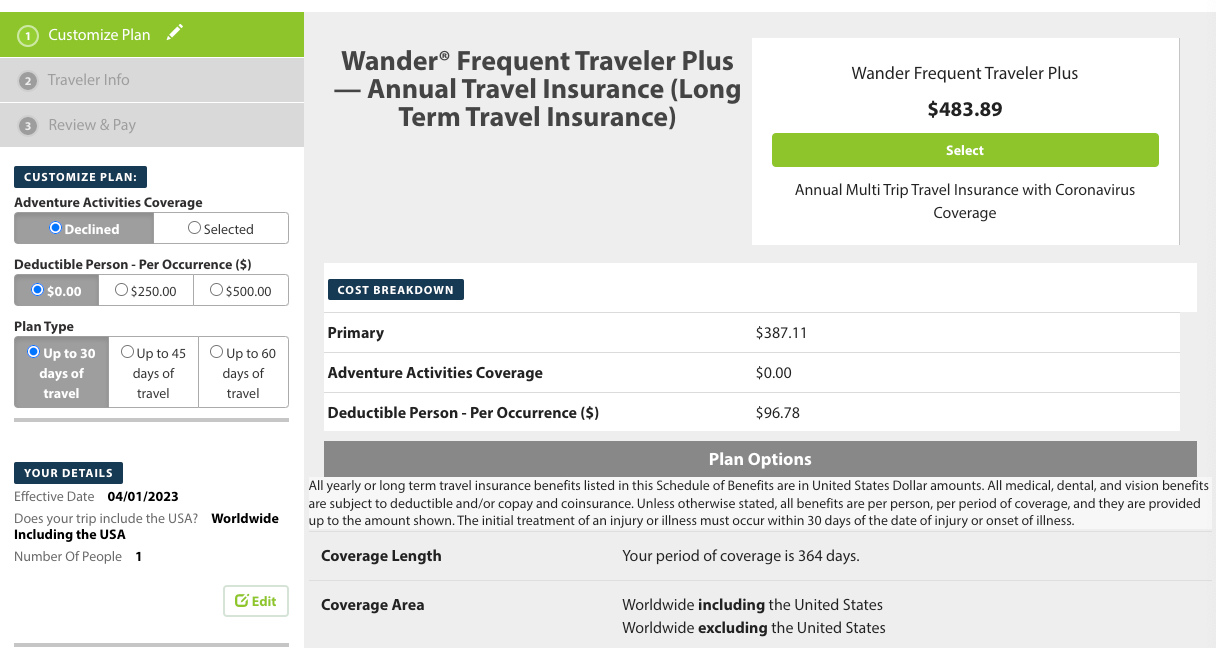

Annual multi-trip insurance.

Santander's Annual Multi-Trip Insurance is designed for those who love to jet-set whenever the travel bug bites. With a solid 4-star rating from fairerfinance.com, you can trust that Santander has got your back. Here are some highlights:

- Medical Excess : Santander offers cover up to £75 towards medical expenses should the need arise during your trip. It's always reassuring to know that you're protected should an unexpected medical emergency occur.

- Personal Possessions and Baggage : If your possessions are damaged, lost, or stolen, Santander provides cover up to £2,000, keeping your belongings safe and sound.

- Cancelling before Travel : It's not always possible to predict the future, which is why Santander offers protection up to £5,000 if you need to cancel your trip before it even begins.

- Emergency Medical and Repatriation : With unlimited cover, Santander ensures you receive the necessary medical care and helps you get back home if needed, so you can focus on getting better.

- Mental Health Cover : While Santander doesn't currently provide specific cover for mental health issues arising on your trip, it's always worth considering your personal circumstances and discussing it further with the insurer.

- Personal Money : If your personal money is lost or stolen, Santander offers cover up to £500, giving you peace of mind wherever you go.

- Additional Benefits : Santander also provides cover for cutting your trip short, abandoning your trip due to delays, relocation costs in natural disasters, and baggage cover during natural disasters.

Single Trip Insurance

If a single holiday is more your style, Santander's Single Trip Insurance is tailored just for you. With excellent ratings and similar benefits to the Annual Multi-Trip option, you can expect the same trust and reliability from Santander. Highlights of this policy include:

- Cancelling before Travel : As with the Annual Multi-Trip Insurance, Santander provides cover up to £5,000 for cancellation before your trip commences.

- Medical Excess : Covering medical expenses up to £75, Santander ensures you receive the care you need while abroad.

- Personal Possessions and Baggage : Up to £2,000 is covered for any damaged, lost, or stolen personal belongings, keeping your holiday stress-free.

- Cutting Trip Short : Unexpected events can sometimes force us to cut our trips short. Santander offers cover up to £5,000 to help manage any additional expenses.

- Missed Departure Cover : If you miss your initial departure, Santander provides financial coverage for your travel arrangements up to £1,000.

Santander Travel Insurance Add-Ons

Santander goes the extra mile by offering two optional add-ons to enhance your coverage for specific types of trips:

- Cruise Cover : Are you planning a cruise? Santander's 3-star rated Cruise Cover safeguards your trip with features such as missed port departure cover, re-joining a cruise cover, and cabin confinement cover. While other benefits may be useful, it's essential to evaluate whether this add-on aligns with your individual needs.

- Winter Sports : Ski season enthusiasts will appreciate Santander's 4-star rated Winter Sports add-on. With features like cover for ski equipment, avalanche closure cover, and piste closure cover, you can hit the slopes with confidence.

Santander Travel Insurance offers a comprehensive range of policies to suit every type of traveller. With convenient options like Annual Multi-Trip and Single Trip Insurance, as well as add-ons for cruises and winter sports, Santander has your back through every journey. While it's always crucial to read the policy documents to understand the finer details, Santander's fairerfinance.com ratings provide assurance of their commitment to customer satisfaction. So, no matter where your wanderlust takes you, be sure to consider Santander Travel Insurance for a worry-free adventure.

Disclaimer: Please note that the information provided in this article is accurate at the time of writing and subject to change. Always refer to Santander's official website for the most up-to-date details on their travel insurance policies.

Sign up for more like this.

The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

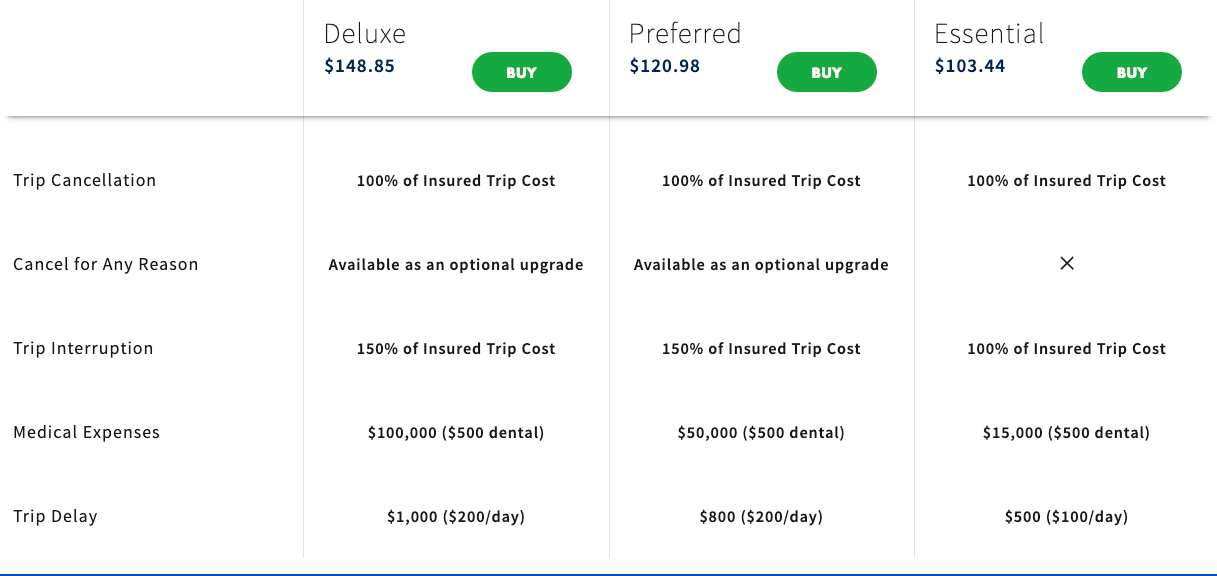

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

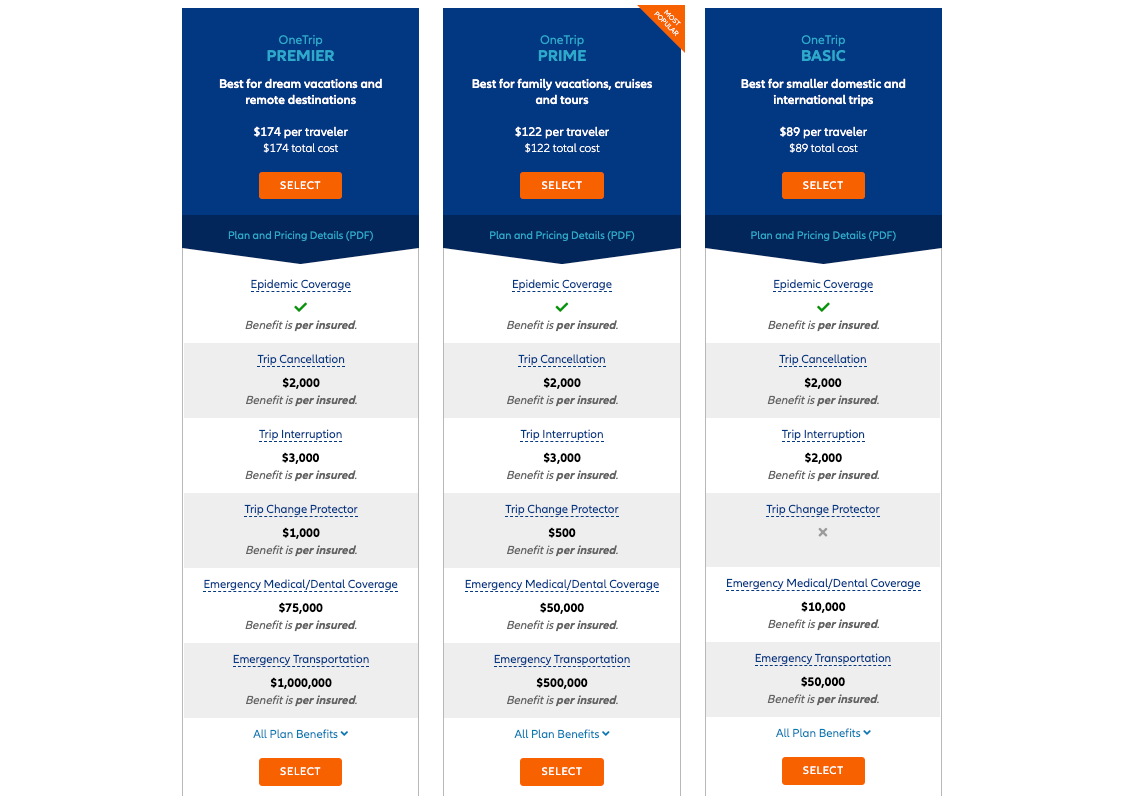

Allianz Travel Insurance

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

American Express Travel Insurance

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

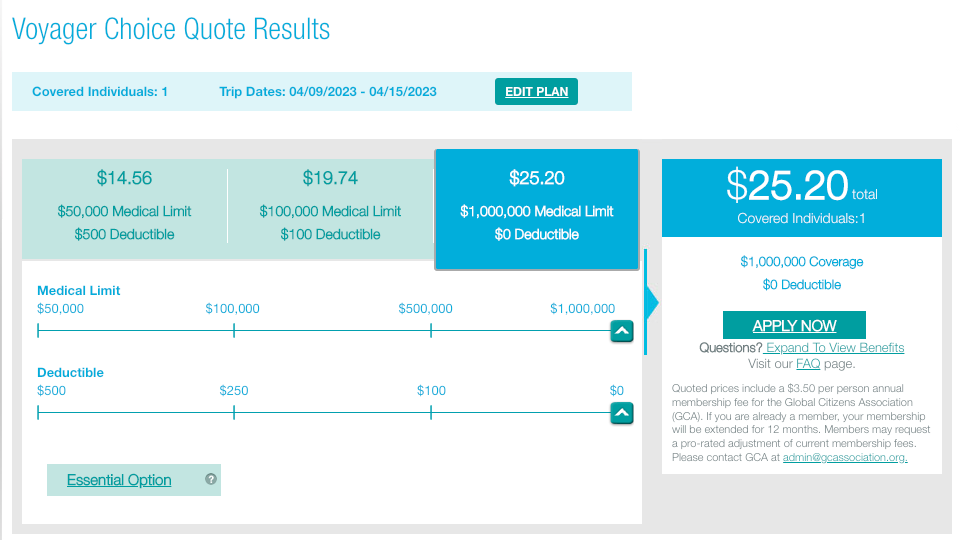

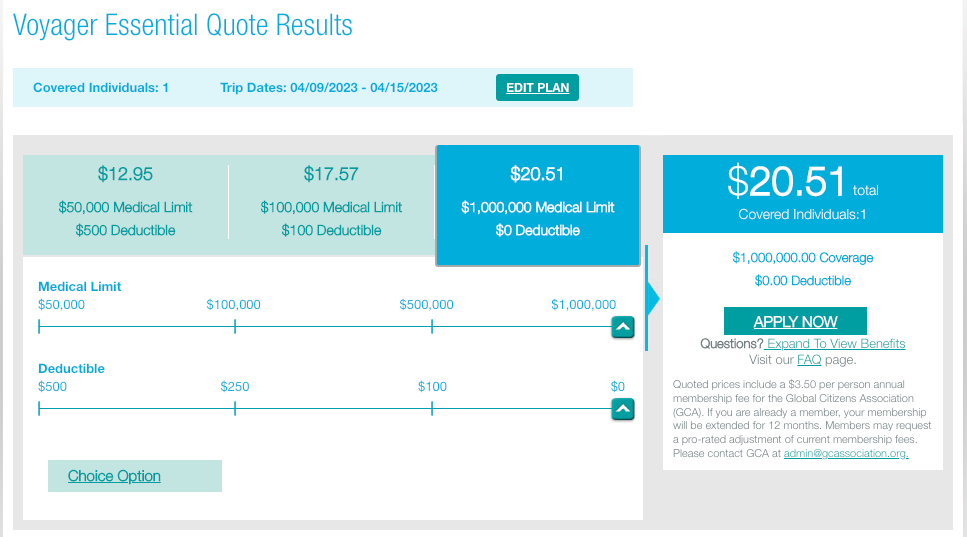

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

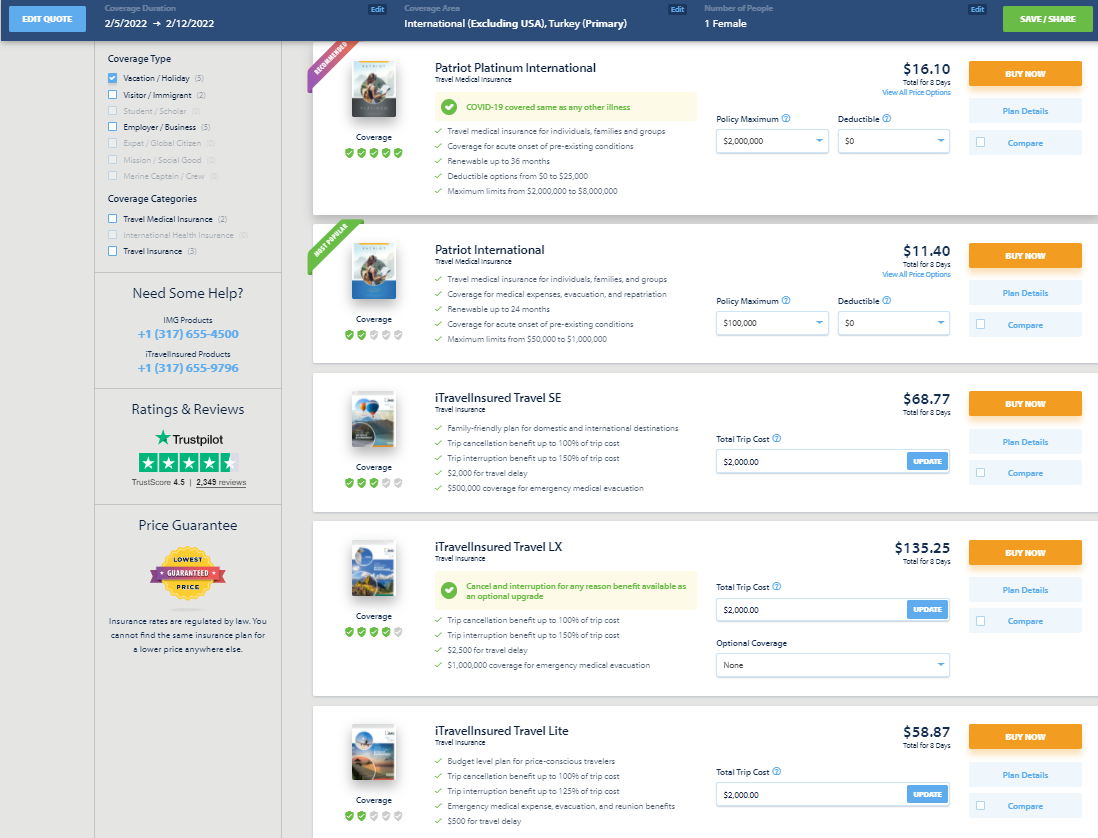

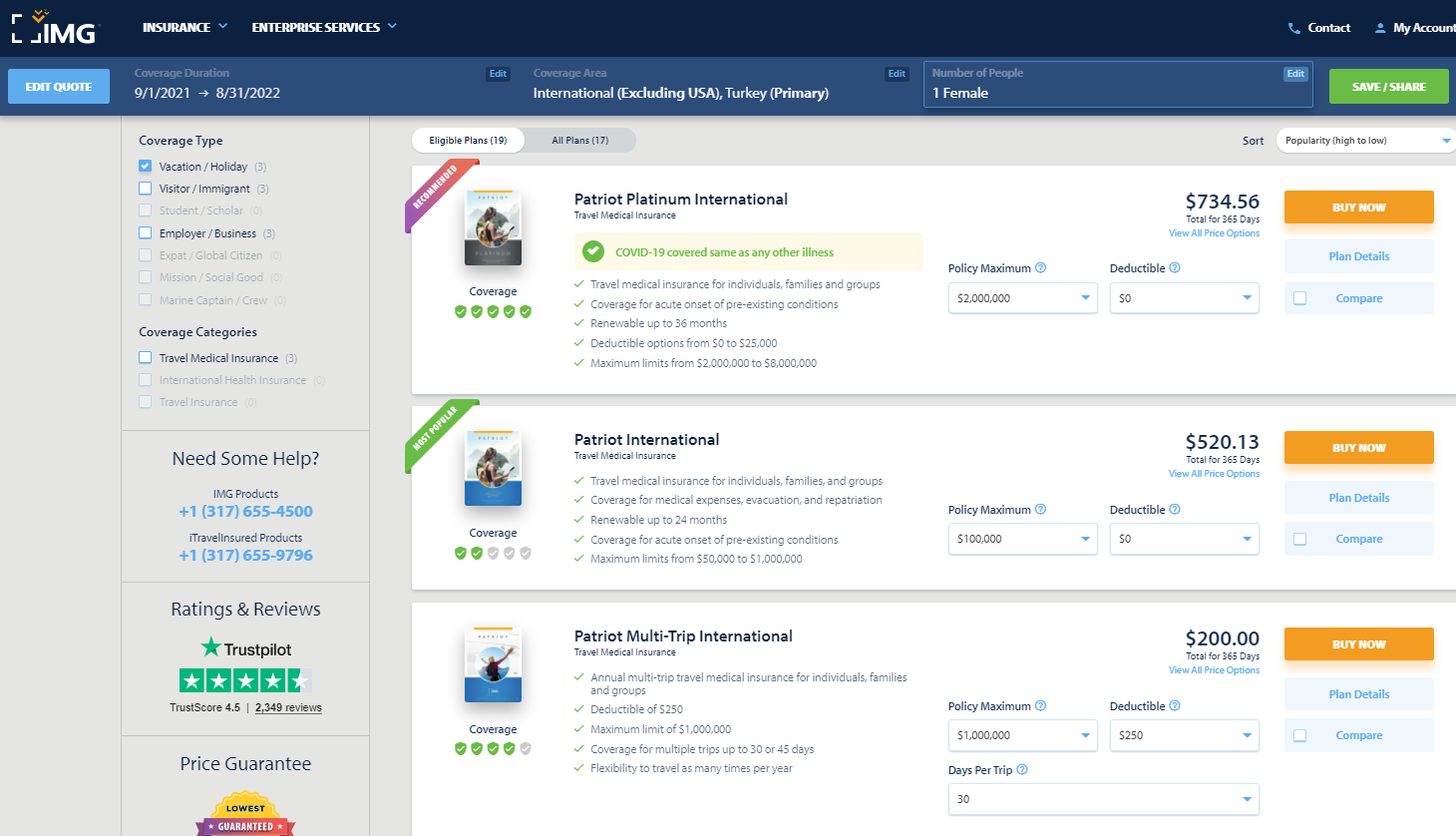

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

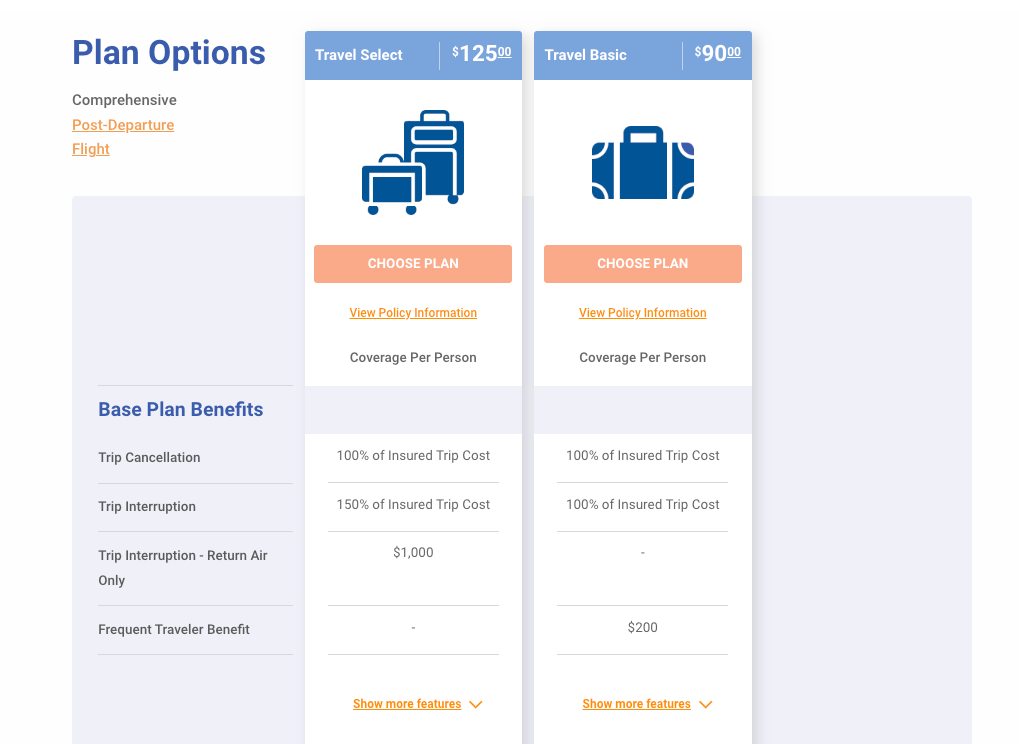

Travelex Insurance

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

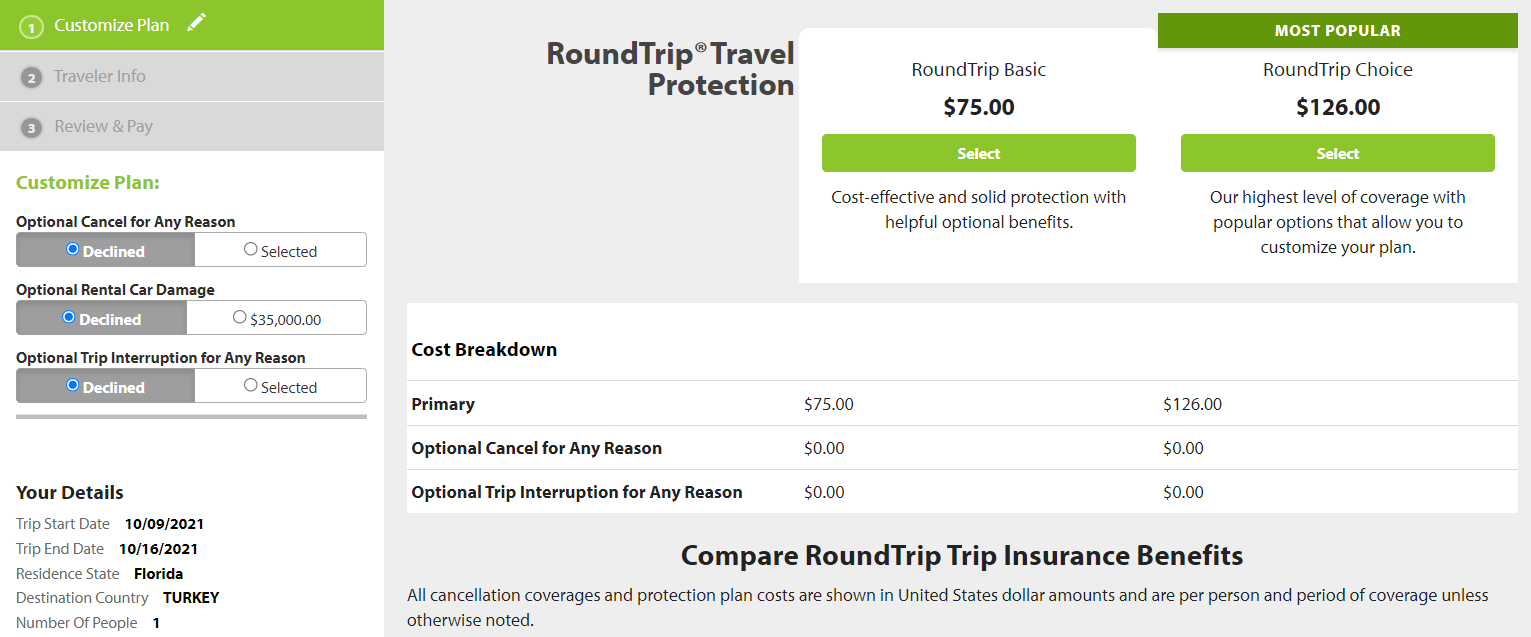

Seven Corners

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

Does the Santander 123 Account Have Travel Insurance?

The Santander 123 Account is one of the most popular bank accounts offered by Santander Bank. It comes with a range of benefits, including cashback on everyday purchases, no monthly fees and competitive interest rates.

One of the key features that makes this account unique is its travel insurance. Santander offers a complimentary Travel Insurance when you open a 123 Account.

The Travel Insurance provided by Santander is comprehensive and includes cover for medical expenses, loss or damage to personal items and luggage, as well as personal liability. It does not cover pre-existing medical conditions, so it’s important to check what these are before you travel. The policy also provides cover for cancellation or curtailment of your trip if your circumstances change unexpectedly.

It’s also worth noting that the Travel Insurance only applies when you use your Santander 123 card to make payments abroad or while travelling. It does not include any protection against theft or accidental damage within the UK.

So, does the Santander 123 Account have travel insurance?

The answer is yes – the Santander 123 Account does come with travel insurance as a complimentary benefit. The policy provides comprehensive cover for medical expenses and loss or damage to personal items and luggage while travelling abroad.

It’s important to note that this insurance only applies when you use your Santander 123 card to make payments abroad or while travelling, and doesn’t include any protection within the UK. Be sure to read through the policy details carefully before you travel so that you’re aware of any exclusions and limitations.

Conclusion:

2 Related Question Answers Found

Does my natwest account have travel insurance, does my natwest account include travel insurance.

Are Travel Trailer Tires Different From Car Tires?

Are Used Travel Trailer Prices Going Up?

© 2023 TravelNow

- Travel insurance

Single trip travel insurance

One off cover to suit your travel needs.

Arranged, administered and underwritten by Chubb European Group SE (CEG).

Award-winning Travel Insurance

As voted by The Times Money Mentor Awards 2023

What is single trip travel insurance?

If you’re planning on travelling only once in the next 12 months, then single trip travel insurance could be for you.

With single trip travel insurance:

- there’s no upper age limit on single trip policies

- it can help protect you for any unplanned events, and

- you can also choose to add optional extensions at an extra cost (including winter sports, cruise, golf and business).

Single trip travel insurance is part of our travel insurance. You can choose to take out either single trip or annual travel insurance cover to suit your needs.

To get a quote, visit our travel insurance page

Single trip travel cover benefits

Rated 5 star in 2023

for quality by Moneyfacts.

Online discount

Santander customers get a 30% discount when applying online.

Unlimited medical cover

We’ll cover the cost of medical treatment while you’re abroad if you get sick or injured. Limitations and exclusions may apply.

How does single trip travel insurance work?

- Single trip travel insurance covers you for one trip of your choice and ends when you come home.

- It’s usually cheaper to take out cover for one journey rather than buying an annual travel insurance policy. However, if you do plan on making more than one trip a year, then annual travel insurance could be more cost-effective.

- You can choose between a European or worldwide policy.

- There’s no age limit.

- It covers you for up to 31 days .

- Single trip cover is part of our travel insurance. To get single trip cover, you’ll need to get a quote for travel insurance. You’ll then have the option to choose between single or annual cover.

The best time to get travel insurance is as soon as you book your trip, as cancellation benefits will begin as soon as the policy starts.

Get a quote

What's covered by single trip travel insurance?

If your luggage is lost, damaged or stolen, we’ll pay up to £2,000 for repair and replacement costs if your luggage is damaged, lost or stolen. the amount of £2,000 relates to personal property, with a single item limit of £300. this excludes money, passports or valuables left unattended (unless locked away). we’ll also pay £200 if it was delayed for at least 12 hours on your outward journey., if you have to cancel or cut your trip short.

We’ll pay up to £5,000 if you have to cancel your trip or cut it short due to circumstances you were unaware of when you took out the policy. We’ll refund the cost of travel, accommodation and any pre-paid tours you didn’t use. We’ll also pay for accommodation and travel to get you home to the UK. We’ll only do this if someone you’re travelling with dies, or suffers a serious injury or illness.

If you get sick or injured

We’ll cover the cost of medical treatment while you’re abroad if you get sick or injured. Any medical treatment you receive must be within a year of the injury or illness first happening. Limitations and exclusions may apply.

No maximum age limit

Unlike some annual travel insurance policies, there’s no upper age limit when it comes to booking a single trip.

To see what’s not covered by travel insurance, take a look at the table on our travel insurance page

Looking for ways to save on insurance?

Our collaboration with insurify may help you save money and find the auto and home coverage that meets your needs..

Get a Quote from Insurify

40+ top insurance companies

View side-by-side quotes from top insurance companies to help you decide what’s best for you.

Quick and easy

In less than five minutes, get accurate personalized quotes in real time.

What you see is what you get

Compare real quotes in one place and choose the best option for you.

Buy online or over the phone

Get the policy you want the way you want it. Buy online or schedule a call with an agent.

Compare quotes with Insurify from top-rated companies

Insurance providers shown are a representative sample:

Insurance products and services described are offered by Insurify Insurance Agency, Inc., not Santander Consumer USA Inc. or its affiliates. Insurify will help you to arrange your insurance needs with selected insurance carriers. Customers of Santander Consumer USA Inc. are not required to purchase an insurance policy through Insurify or any specific insurance company in connection with their auto loan or lease, and your choice of agent or insurer shall not affect any credit decision or credit terms except as related to the credit worthiness of the insurer and the scope of coverage. Insurify may compensate Santander Insurance Agency US LLC if you sign up for insurance through Insurify. Insurify Insurance Agency, Inc. is a licensed insurance agency in 50 states and DC.

According to Insurify, all insurance carriers are at least A-rated by Standard & Poor’s or equivalent. Products may not be available in all states.

Benefits - Santander

First time user? Enroll now!

Forgot User ID?

Forgot Password?

- Retail Online Banking

- Mortgage Accounts

- Business Online Banking

- Investment Services

- Consumer Credit Cards

Navigation Menu

Welcome to Santander ® Private Client

Enjoy our highest level of benefits and our utmost care and attention.

You have ambitions, we’ll help you achieve them.

We’re honored to be a part of your legacy. as a santander private client, your goals are put into the care of our most experienced bankers and financial specialists. this is just the beginning, we can’t wait to help you achieve your lifetime aspirations..

Santander Private Client benefits

Exclusive perks.

- An array of no-fee banking services that include complimentary official bank checks, stop payments, incoming wire transfers, overdraft protection transfers, and more For additional details, please refer to the Santander Private Client Fee Schedule

- Save more when using your Santander Private Client® World Debit Mastercard® at home or abroad 1,2

Secure access

- Trust Santander PROTECHTION for Mobile and Online Banking with confidence and control

- Manage your accounts using digital controls for cards, alerts, and more

- Bank with digital confidence using biometric authentication: Face ID®, Touch ID for Apple devices, and fingerprint authentication for Android 3

Easy management tools

- Bank from anywhere with our Mobile Banking App and Online Banking

- Send and receive money easily with Zelle®

- Higher ATM and debit card purchase and withdrawal limits

Tailored services

- Guidance from a team of financial specialists in investments*, home lending, and business banking

- Access to a Santander Investment Services* Financial Advisor who will work with you to develop and adjust your financial plan using MoneyGuidePro®, a premier provider of financial planning software

- Financial education events and digital resources to help you take charge of your financial future

Special travel and entertainment services

- Access to exclusive tickets and reservations with Mastercard Concierge Services

- Travel and purchase protections with the Santander Private Client World Debit Mastercard®

- Complimentary standard membership to Priority Pass, the world’s leading airport lounge program. Enroll today at prioritypass.com/santander , invitation code: 6782266

- For additional assistance call the Santander Private Client World Debit Mastercard Benefits Line at 1-866-214-5084 .

Call us today

Priority service and support.

Santander Private Client Services

For additional details, please refer to the Santander Private Client Fee Schedule and our Personal Deposit Account Agreement . 1. No international transaction fee for debit card purchases and ATM withdrawals. 2. All ATM surcharge fees charged by other institutions at non-Santander ATMs will be rebated. The rebate is posted the Business Day after the fee is charged and is reported as miscellaneous income subject to tax reporting. 3. If you share your device with other individuals, please note any fingerprints or face image stored on your device may be used to log in to the Santander Mobile Banking App and access your account. *Securities and advisory services are offered through Santander Investment Services, a division of Santander Securities LLC. Santander Securities LLC is a registered broker-dealer, Member FINRA and SIPC and Registered Investment Adviser. Insurance is offered through Santander Securities LLC or its affiliates. Santander Investment Services is an affiliate of Santander Bank, N.A.

Personal Banking Investing Small Business Commercial Private Client

Careers Our Commitment Leadership Media Center Shareholder Relations Work Café

Servicemembers Civil Relief act (SCRA) Benefits Help For Homeowners Having Difficulty Paying Their Mortgage

Find a Branch/ATM Personal Banking Resources Small Business Resources Security Center Site Map

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

7 Best Cheap Travel Insurance Companies in April 2024

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

Finding the cheapest travel insurance is often a priority for travelers hoping to protect themselves and their finances while away from home.

But is it better to err on the side of affordable travel insurance or opt for a more comprehensive plan? That depends on your needs .

On average, a comprehensive plan that covers some combination of trip cancellation and interruption costs, medical coverage and baggage protection (and perhaps a number of other things) will cost you 5%-10% of what you paid for the trip, according to NerdWallet partner Squaremouth, a travel insurance marketplace.

That means a comprehensive policy for a trip that costs you $3,000 could run you anywhere between $150 and $300. Factors like the cost and length of your trip, the age of the travelers and how much protection you want can significantly influence what you pay for your plan.

Ultimately, Squaremouth recommends “the least expensive policy that offers the coverage [travelers] need.”

» Learn more: The best travel insurance companies right now

Factors we considered when picking cheap travel insurance plans

We considered a few factors as we looked for the most affordable travel insurance plans.

Price: If your goal is to find cheaper travel insurance, you want the price to be affordable.

Breadth of coverage: The best budget travel insurance is typically going to be a plan that offers a wide range of protections at an affordable cost, ensuring you’re protected with at least some coverage for a wide range of scenarios.

Uniqueness or customizability : While many travel insurance plans have similar protections, some stand out for particular coverage that can be helpful to certain travelers, like those needing to Cancel For Any Reason , those going on a cruise, or travelers with preexisting health conditions. We didn’t spring for the priciest plans with broad, deep coverage; instead, we picked those that meet a sort of budget "sweet spot" when it comes to cost efficiency.

» Learn more: Is travel insurance worth getting?

An overview of the best cheap travel insurance plans

We looked at travel insurance quotes for a hypothetical 10-day trip to Italy in October 2023. The traveler is a 40-year-old man living in North Carolina who spent $2,000 on the trip, including airfare.

Reliable but cheap travel insurance providers

1. axa assistance usa (silver plan: $70).

Why we picked it:

The $500 missed connection benefit is great for cruise and tour participants. It covers additional transportation, accommodations and meal costs when you miss a cruise or tour departure.

Full trip cancellation and interruption coverage, along with up to $25,000 for out-of-pocket medical costs and baggage coverage.

Among the lowest prices we found.

If you’re willing to spend a bit more than AXA's $70 Silver plan, a Gold plan only costs $19 more and gets you deeper coverage amounts and up to $35,000 in collision rental car insurance.

2. Berkshire Hathaway Travel Protection (ExactCare Value plan: $56)

Cheapest plan we found while still offering a wide array of protections.

Includes a preexisting medical condition waiver.

Add-on rental car collision coverage optional for $10 per day. You can pick how many days you want the additional coverage — it’s not all or nothing.

At $56, this plan comes in at less than 3% of the $2,000 trip cost.

3. IMG (iTravelInsured Lite plan: $77)

Treats COVID-19 like any other illness, which is to say, if your claim accepts flu, strep throat or appendicitis as an acceptable, covered condition, the coronavirus is, too.

Covers costs related to trip interruption up to 125%

Higher than normal limits on dental expenses, at $1,000. If your teeth are your Achilles heel (or your biggest fear), this plan might be for you.

The iTravelInsured Lite plan doesn’t offer some of the bells and whistles that other plans do, like rental car coverage , Cancel For Any Reason coverage or waivers for pre-existing conditions. But you’ll have relatively solid across-the-board trip protections.

4. John Hancock (Silver plan: $93 for a mid-tier plan)

Mid-level plan (as opposed to a basic plan) at an affordable price for travelers who want more coverage without paying too much.

Includes an optional Cancel For Any Reason add-on for travelers wanting flexibility. It is a bit pricey, at half the cost of the insurance ($46.50 extra for a $93 plan).

Reimburses up to $1,000 for lost baggage , far more than many basic plans.

Add-on rental car coverage for $9 per day.

At $88, John Hancock’s basic (Bronze) plan isn’t particularly affordable. But for just $4 extra, you can tap into the benefits of a mid-tier plan at still less than 5% of the total trip cost.

5. Nationwide (Essential plan: $76)

Includes a preexisting conditions waiver.

Add-on rental car coverage for $90.

Covers trip interruption at 125% of the trip cost while providing comprehensive emergency medical and baggage coverage.

6. Seven Corners (Basic plan: $75)

On top of standard trip protections, it includes a relatively affordable Cancel For Any Reason option for $31.50 extra.

If you plan to rent expensive sporting equipment, you might consider paying $10 extra to cover lost, damaged, stolen or destroyed gear.

COVID-19 coverage reimburses you for costs incurred if you have to quarantine .

Rental car coverage comes in at an affordable $7 per day.

Seven Corners’ Basic plan stands out because it offers a little bit of everything, appealing to athletic travelers, those who need affordable trip protections, those who want the flexibility to cancel for any reason and those still concerned about getting quarantined due to COVID-19.

7. Travelex Insurance Services (Basic plan: $71)

Straightforward: What you see is what you get. This plan’s coverage has fewer rules and caveats than many.

While not sporting the highest coverage amounts, it offers a solid range of protections to ensure you get at least something back when your travel is disrupted or you have a medical emergency.

Offers add-on rental car coverage for $10 per day.

At $71, the Travelex Basic plan’s cost is just over 3% of the $2,000 trip’s cost.

If you want to get travel insurance at the cheapest possible rate, here’s a trick. Put $0 as your trip cost, Stan Stanberg, co-founder of comparison site Travelinsurance.com said in an email.

“When excluding trip cancellation and trip interruption coverage the cost of a travel insurance plan goes down significantly,” Stanberg said.

That means you won’t get reimbursed if you need to cancel your trip or if it gets interrupted. But you may still have access to the plan’s medical, trip delay , missed connection, baggage and other protections.

You’ll often find comprehensive travel insurance plans cost 5%-10% of your total trip cost, according to Squaremouth. This will often get you full trip cancellation and trip protection, baggage protection, emergency medical coverage and often other benefits.

Typically, the more you pay, the broader and deeper the coverage.

For many plans, you can purchase travel insurance up until you depart. However, to get access to the most protections possible, booking two days to two weeks after making your initial deposit is the best rule of thumb.

That means you won’t get reimbursed if you need to cancel your trip or if it gets interrupted. But you may still have access to the plan’s medical,

, missed connection, baggage and other protections.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2024 , including those best for:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

on Chase's website

1x-10x Earn 5x total points on flights and 10x total points on hotels and car rentals when you purchase travel through Chase Travel℠ immediately after the first $300 is spent on travel purchases annually. Earn 3x points on other travel and dining & 1 point per $1 spent on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $900 toward travel when you redeem through Chase Travel℠.

1x-5x 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $750 when you redeem through Chase Travel℠.

1x-2x Earn 2X points on Southwest® purchases. Earn 2X points on local transit and commuting, including rideshare. Earn 2X points on internet, cable, and phone services, and select streaming. Earn 1X points on all other purchases.

50,000 Earn 50,000 bonus points after spending $1,000 on purchases in the first 3 months from account opening.

Share tips of the week – 26 April

MoneyWeek’s comprehensive guide to the best of this week’s share tips from the rest of the UK's financial pages.

Revealed: the countries with the most generous pensions

State pension errors: DWP urged to check for mistakes among divorced people

Should you invest in UK equities?

Buyers need to earn £20k above average UK salary to afford sold house prices, Go.Compare finds

Private school fees soar and VAT threat looms – what does it mean for you?

The MoneyWeek Readers' Choice Awards 2024

Sign up to money morning.

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Most Popular

The FTSE 100 hit a record high this week, but UK equities remain unloved and undervalued compared to their global and US peers. Should you snap them up at a discount?

The UK state pension is often criticised for failing to deliver a comfortable retirement. So, how does our pension system compare to other countries - which countries are most generous, and at what age can you claim a state pension?

The best one-year fixed savings accounts – April 2024

Savings Earn nearly 6% on one-year fixed savings accounts – the best rate seen in 14 years. We have all the best deals available now

Share tips of the week

Tips MoneyWeek’s comprehensive guide to the best of this week’s share tips from the rest of the UK's financial pages.

MoneyWeek Awards The MoneyWeek Readers' Choice Awards celebrate the products and services that help you make, keep and spend your money. Vote now in the 2024 awards.

News The average UK salary is £20k too low to afford the country's typical house price - we look at just how much you need to earn to step onto the property ladder in the UK

AstraZeneca CEO’s £1.8mn pay rise approved despite shareholder opposition

AstraZeneca hiked its dividend to persuade shareholders to accept CEO Pascal Soriot’s pay rise. Is he worth his salary?

Adidas, Nike or Jordans - could collectable trainers make you rich?

The right pair of trainers can fetch six figures. Here's how you can start collecting vintage Adidas, Nike or Jordans now

By Chris Carter Published 22 April 24

Investors are snapping up gilts thanks to tax incentives – but is your money better off elsewhere?

UK government bonds, also known as gilts, are proving popular with investors so far this year, thanks to higher interest rates and the attractive tax incentives they offer. Should you invest in them?

By Katie Williams Published 22 April 24

What is bitcoin halving and what does it mean for crypto investors?

The latest bitcoin halving event took place in the early hours of Saturday morning. Historically, this practice has caused the cryptocurrency to soar in value. What’s happening with the bitcoin price this time?

By Katie Williams Last updated 22 April 24

Personal Finance

Coventry Building Society bids £780m for Co-operative Bank - what could it mean for customers?

Coventry Building Society has put in an offer of £780 million to buy Co-operative Bank. When will the potential deal happen and what could it mean for customers?

RBS to close a fifth of branches

Royal Bank of Scotland plans to shut 18 branches across Scotland, resulting in the loss of 105 jobs. We have the full list of closures.

By Ruth Emery Published 18 April 24

State pension warning as families opting out of child benefit hits record high

Up to one million parents could be losing out on £6,500 in retirement because they have opted out of receiving child benefit.

Barclays warns of significant rise in social media investment scams

Investment scam victims are losing an average £14k, with 61% of those falling for one over social media. Here's how to spot one and keep your money safe

By Oojal Dhanjal Published 17 April 24

UK inflation slowed again in March – but a rate cut could be some months away

The latest Consumer Price Index (CPI) data came in at 3.2% for March. This was slightly higher than some economists expected, but takes us closer to the Bank of England’s 2% inflation target.

ONS wage growth data puts Bank of England UK interest rate cuts into doubt, analysts warn

News ONS wage growth data has shown earnings are continuing to rise at an inflation-busting rate. It means cuts to the base rate may come later in the summer

By Henry Sandercock Published 16 April 24

What does conflict in the Middle East mean for oil prices and the economy?

Israel launched a retaliatory strike on Iran in the early hours of Friday morning. Oil prices spiked in response, before falling back again. As tensions escalate, what’s next for inflation and the economy?

By Katie Williams Last updated 19 April 24

UK sold house prices fall again amid mortgage rates uncertainty, ONS House Price Index shows

News The latest Office for National Statistics (ONS) analysis of UK sold house prices data showed they remained down year-on-year.

Pension vs property: which option provides the best income for your retirement?

News With the cost of a comfortable retirement on the rise, future retirees need to weigh up which strategy offers the best returns. But is a pension a better bet than property?

Most expensive street in Britain to buy on has houses with '£10m average asking price', Rightmove finds

News Rightmove found Buckingham Gate, close to Buckingham Palace, was the most expensive street in the country. Do you live near one that's been included on the list?

By Henry Sandercock Published 15 April 24

- Money Masterclass

Should you sell in May this year?

The market adage looks unlikely to apply in 2024, and global equities are proving resilient. Should you sell in May?

Best and worst UK banks for online banking revealed

When it comes to keeping your money safe, not all banks are equal. We reveal the best and worst banks for online banking when it comes to protecting your money from scams

By Oojal Dhanjal Published 24 April 24

Stop inheritance tax perk on pensions, says IFS

The government could raise billions of pounds in revenue by closing inheritance tax loopholes, such as on pensions and AIM shares. Is your pension at risk?

By Ruth Emery Published 23 April 24

Revealed: Best buy-to-let property hotspots in the UK

Looking for the best buy-to-let property locations in the UK? We reveal the top 10 postcodes with the strongest rental returns

By Oojal Dhanjal Published 23 April 24

Meet the team

Kalpana Fitzpatrick

Marc Shoffman

Katie Williams

Vaishali Varu

Henry Sandercock

Useful links.

- Subscribe to MoneyWeek

- Get the MoneyWeek newsletter

- Latest Issue

- Financial glossary

- MoneyWeek Wealth Summit

- Best savings accounts

- Where will house prices go?

- Contact Future's experts

- Terms and Conditions

- Privacy Policy

- Cookie Policy

- Advertise with us

Moneyweek is part of Future plc, an international media group and leading digital publisher. Visit our corporate site . © Future Publishing Limited Quay House, The Ambury, Bath BA1 1UA. All rights reserved. England and Wales company registration number 2008885.

Advertiser Disclosure

Many of the credit card offers that appear on this site are from credit card companies from which we receive financial compensation. This compensation may impact how and where products appear on this site (including, for example, the order in which they appear). However, the credit card information that we publish has been written and evaluated by experts who know these products inside out. We only recommend products we either use ourselves or endorse. This site does not include all credit card companies or all available credit card offers that are on the market. See our advertising policy here where we list advertisers that we work with, and how we make money. You can also review our credit card rating methodology .

For the Frequent Traveler: The 11 Best Annual Travel Insurance Policies

Content Contributor

66 Published Articles

Countries Visited: 197 U.S. States Visited: 50

Jessica Merritt

Editor & Content Contributor

84 Published Articles 483 Edited Articles

Countries Visited: 4 U.S. States Visited: 23

Keri Stooksbury

Editor-in-Chief

33 Published Articles 3136 Edited Articles

Countries Visited: 47 U.S. States Visited: 28

GeoBlue Trekker Choice

Geoblue trekker essential, trawick international safe travels annual basic, trawick international safe travels annual deluxe, allianz travel alltrips basic plan, allianz travel alltrips prime plan, allianz travel alltrips executive plan, allianz travel alltrips premier plan, aig travel guard annual travel insurance plan, usi affinity voyager annual travel insurance, seven corners travel medical annual multi-trip, a plan that didn’t make our list, how annual travel insurance works, when to buy an annual travel insurance policy, what annual travel insurance policies do and don’t cover, understanding trip length rules, is annual travel insurance worth it, how much do annual travel insurance policies cost, does credit card travel insurance apply annually, choosing an annual travel insurance policy, final thoughts.

We may be compensated when you click on product links, such as credit cards, from one or more of our advertising partners. Terms apply to the offers below. See our Advertising Policy for more about our partners, how we make money, and our rating methodology. Opinions and recommendations are ours alone.

If you take multiple trips every year, insuring each one can be a hassle. There are forms to fill out, comparison shopping over and over again, and then remembering the policy documents for each specific trip. And then there’s the risk you might forget to take out travel insurance for one of your trips.

Plus, those costs add up. There must be a better way.

Enter annual travel insurance. Also known as multi-trip travel insurance, taking out an annual policy covers you for a whole year of travel. Not only is it simpler, it may be cheaper than taking out multiple single-trip policies. But is it right for you?

Annual travel insurance policies aren’t exactly the same as the trip insurance you’d buy for a weeklong holiday with your family. Here are the best annual travel insurance policies, what they do and don’t cover, and how to decide whether taking out a yearly policy might be right for you.

The 11 Best Annual Travel Insurance Policies

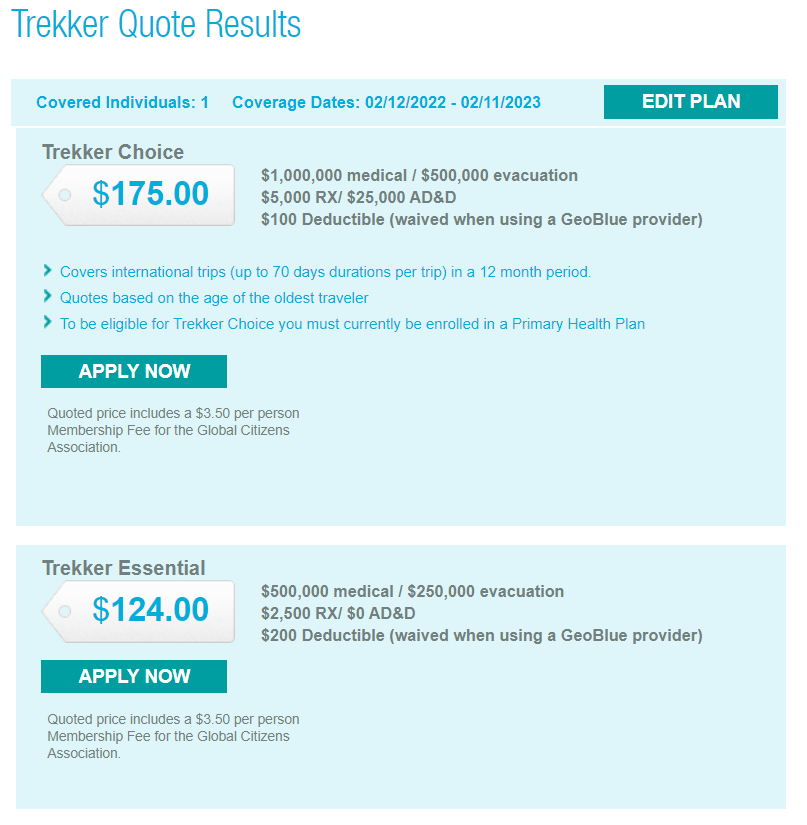

GeoBlue offers 2 Trekker plans for annual coverage, which are unique in several ways. These plans cover preexisting conditions, COVID-19, and all travel outside the U.S.

However, they don’t cover any trips inside the U.S. or provide any coverage for canceled, delayed, or interrupted trips. Instead, these are travel medical insurance plans . With the GeoBlue Trekker Choice plan , you’ll get higher maximum payouts in all categories and pay a lower deductible ($100). However, note that this is still secondary coverage .

You’ll get unlimited access to telemedicine and coverage for trips up to 70 days in length . Additionally, coverage is available up to age 95, which isn’t offered on most other policies.

The GeoBlue Trekker Essential plan offers the same pros and cons as the Choice plan. The main differences are the lower maximum payout values and the higher deductible ($200 instead of $100). You also won’t get the Choice plan’s lost baggage and personal effects coverage, which can provide up to $500 per trip. Again, this secondary medical insurance policy is only valid on trips outside the U.S.

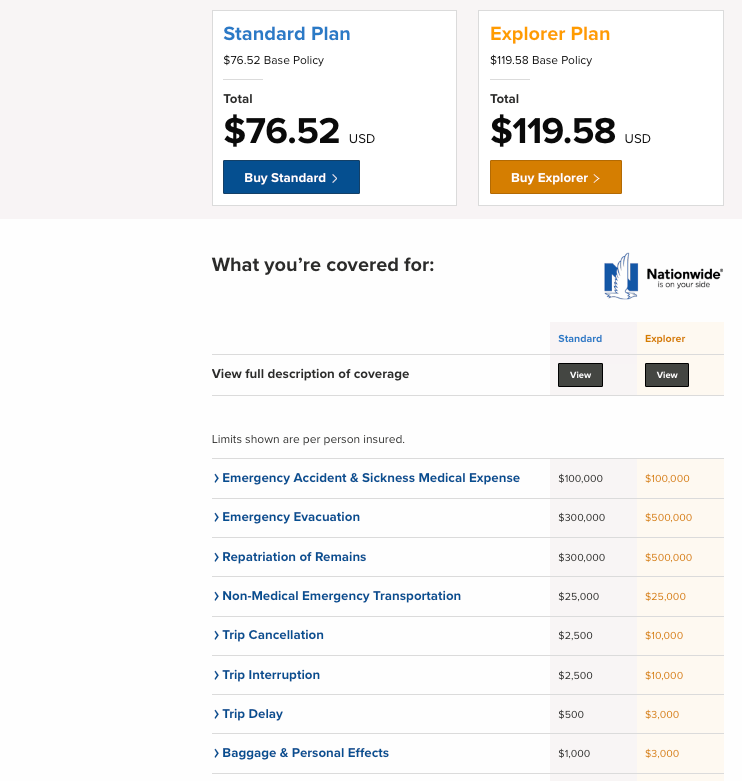

Trawick International offers 2 annual plans, and the Safe Travels Annual Basic plan is more economical. You’ll have coverage for everything you expect in a trip insurance policy , such as 100% coverage for trip cancellation or interruption (up to a $2,500 annual maximum) and coverage for delays, lost luggage, delayed luggage, and even medical expenses. To make up for the lower cost of the plan, coverage limits are lower than what you’ll find elsewhere . However, if you want peace of mind while traveling, you can get it for a year and cover trips up to 30 days in length.

While Trawick International’s Safe Travels Annual Deluxe plan offers higher maximum coverage limits than the Basic plan, its maximum payouts for medical and evacuation benefits are lower than what you’ll find with competitors . Where this plan shines is in the coverage for change fees, lost deposits on tours, and coverage for lost items if an airline misplaces your luggage.

You’ll be covered for up to $300 per trip for prepaid excursions, up to 100% of your trip cost (with an annual maximum of $5,000) for trip cancellations or interruptions, and up to $150 per item and $750 per trip for personal effects. After signing up for a plan, you’ll also get a 10-day free look period.

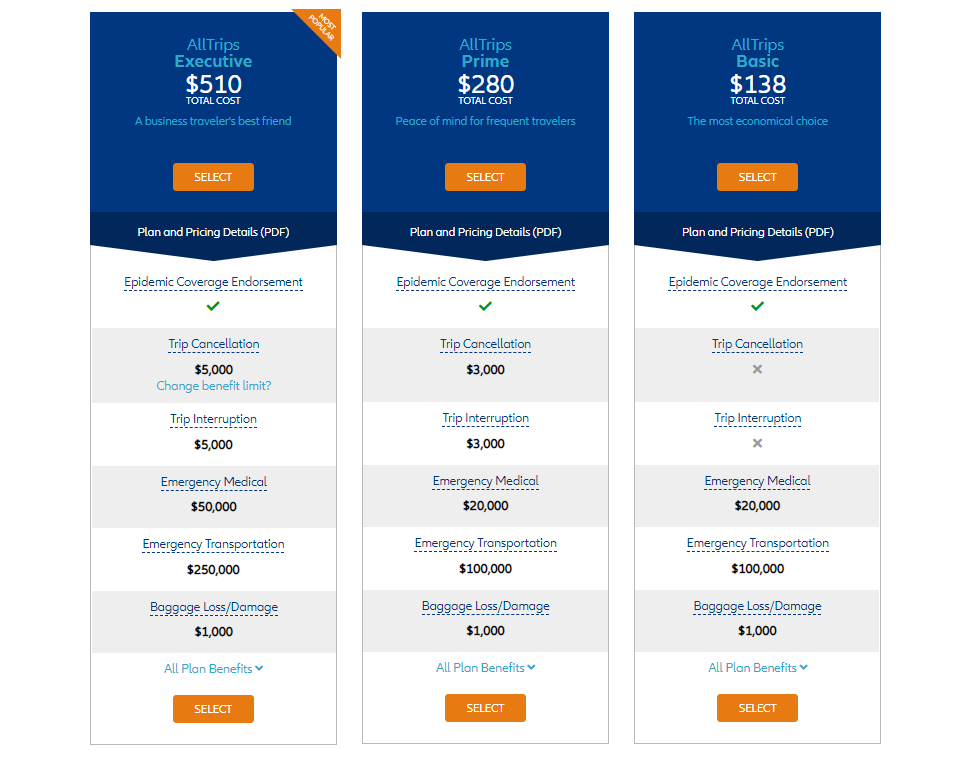

If you want an annual plan with a low price tag , this could be what you’re looking for. The Allianz Travel AllTrips Basic plan covers you for unlimited trips up to 45 days each over the course of a year. Coverage includes emergency medical, emergency medical evacuation, baggage loss and delays, travel delays, rental car theft and damage, and travel accident coverage.

However, there’s a fair list of exclusions from this plan . That includes trip cancellation, trip interruption, missed connections, and change fees. As the name implies, you’ll get basic coverage at a basic price.

The Allianz Travel AllTrips Prime option covers 365 days of trips, though the maximum trip length is just 45 days. While you’ll get coverage for all the standard travel insurance benefits, including trip cancellation, trip interruption, emergency medical, delays, and baggage mishaps, there are limits you should know about with this plan.

The travel accident coverage, which applies to death or the loss of a limb, maxes out at $25,000 per trip, baggage delay maxes out at $200, and baggage loss or damage maxes out at $1,000. The maximum coverage for emergency medical is $20,000, and costs can exceed that quickly in a true emergency.

However, this is a decent option if you want a fair amount of coverage across numerous categories without a high price tag.

For those worried about expensive business equipment or losing points and miles, this plan has you covered. On top of higher maximum payouts in categories such as trip cancellation, emergency medical transportation, or travel delays, you’ll also get rental car damage and theft coverage, change fee coverage, and reimbursement for renting business equipment if yours is lost, stolen, damaged, or delayed during a trip.

Moreover, you can be reimbursed up to $500 to cover fees for reinstating your points and miles if a covered trip is canceled or interrupted. The Allianz Travel AllTrips Executive plan also provides coverage for preexisting medical conditions if you meet certain criteria and buy at least 14 days before the first trip.

Allianz also has a customizable AllTrips Premier plan , allowing you to choose between several payout tiers for trip cancellation and interruption. You’ll pay more when choosing higher maximums, but this allows you to choose exactly what you want in coverage and not pay for more than you need. Another positive is coverage for preexisting medical conditions if you meet certain criteria and buy your policy at least 14 days before your first trip.

You’ll also get rental car damage and theft coverage , $500,000 of emergency medical transportation coverage, $50,000 of emergency medical, and coverage for travel delay expenses after a delay of 6 hours or more. The baggage delay coverage is up to $2,000, but it requires a delay of 12 or more hours. The maximum trip length allowed is 90 days.

The AIG Travel Guard Annual Travel Insurance plan isn’t available to Washington state residents. Still, it provides coverage for trip interruption, trip delay, lost baggage, delayed baggage, and missed connections, as well as both medical and security evacuation, accidental death and dismemberment, and travel medical expenses. However, the coverage limit for dental is just $500, and the maximum coverage for travel medical expenses is just $50,000. Those are lower limits than other plans. Additionally, trip cancellation isn’t included.

However, Travel Guard has some strengths. Trip delay coverage applies for up to 10 days and requires a delay of just 5 hours, and the missed connection benefit applies after just 3 hours. You get a “free look” period of up to 15 days to cancel for a refund, so long as you haven’t started your trip or filed a claim. Maximum coverage for any particular trip is 90 days.

USI Affinity’s Voyager plan has a Silver and Gold option , and pricing is easy to determine from the chart. Simply find your age bracket and the associated cost. The key differences between the plans are in the higher maximum payouts for nearly every coverage type with the Gold plan, other than emergency dental and accidental death and dismemberment. However, the Gold plan also includes coverage types the Silver plan doesn’t: political and natural disaster evacuation, airline ticket change fees, and trip interruption. However, trip cancellation isn’t included with either plan .

The maximum trip length is 90 days, and coverage for Silver and Gold plans lasts for 364 days. An unlimited number of international and domestic trips are covered, and you’re covered for trips as little as 100 miles from home. That’s a lower requirement than most other plans (which tend to require 150 miles).

This plan is ideal for those who don’t live in the U.S., as other plans on this list are only available to U.S. residents and citizens. While the plan technically lasts for 364 days, Seven Corners’ Travel Medical Annual Multi-Trip plan is customizable. It lets you choose a maximum trip length of 30, 45, or 60 days and include or exclude coverage for the U.S. Note U.S. citizens and residents cannot add coverage for inside the U.S.